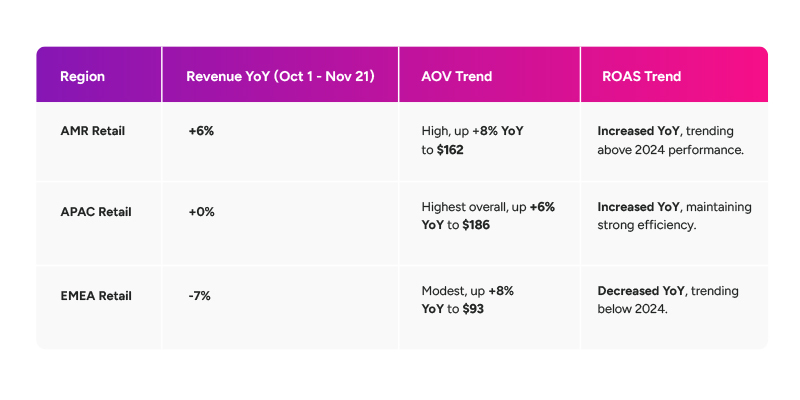

The retail calendar from October 1st to November 21st marks the crucial ramp-up to the Cyber 5, and our latest global data confirms that the momentum is building rapidly. While Singles’ Day served as an initial pulse check, our benchmarks for the expanded period now show a significant acceleration, with global retail revenue growing to +6% Year-over-Year (YoY).

The overall narrative remains clear: shopper behavior has fundamentally changed. Traffic is robust, but conversion is harder-earned. Success hinges entirely on securing higher average order values (AOV) and optimizing based on the highly varied regional performance.

Global Trends: The AOV Lifeline

Across global retail (excluding food & drink), the channel has successfully increased its YoY revenue growth rate since Singles’ Day. This growth has been achieved primarily by drawing higher-intent traffic (+10% Clicks YoY) that delivers greater value per transaction:

AOV: Continues its strong performance, up +9% YoY to $139.

Conversions: Are still a challenge, down -2% YoY (though this is a 4% improvement in the decline rate since the Singles’ Day period).

This trend confirms that consumers are consolidating their purchases, making fewer, but more valuable, transactions. This places a premium on partners who drive high-intent, upper-funnel influence.

The Regional Divide: Who is Driving Growth?

Beneath the global number, performance is driven almost exclusively by the Americas, while other regions face headwinds:

AMR is the Sole Engine: The Americas region continues to be the only consistent driver of global retail growth. Its high AOV and strong return on ad spend (ROAS) performance ensure profitability, offsetting declines elsewhere.

The EMEA Efficiency Challenge: EMEA is the most volatile market. While clicks are surging (+40% YoY), the conversion efficiency is lagging, leading to the -7% revenue decline. Critically, EMEA is the only region where ROAS has decreased YoY. However, the Pre-Thanksgiving window (Nov 20th – 26th) showed promise, with conversion trends beginning to recover and ROAS converging toward 2024 levels, suggesting a potential late recovery.

The ROAS Race: Who is Most Efficient?

ROAS is the clearest indicator of channel health:

- EMEA still maintains the highest absolute ROAS value overall, but the YoY decline indicates a need for strategic intervention to maintain efficiency.

- AMR and APAC are both showing increasing ROAS YoY due to their growing AOV and efficient commission rates. APAC, in particular, has seen a +15% ROAS increase fueled by higher consumer spend and lower commission costs.

Partner Implications for the Cyber 5

The trends confirm that buy-now-pay-later (BNPL) remains a top-tier partner category, consistently ranking highly for both AOV and new customer acquisition. Furthermore, while the global shift favors Influencers (+1.6% share gain), the AMR market is showing a unique counter-trend, leaning heavier into loyalty partners (+3.2% share gain in AMR).

With Cyber 5 now mostly behind us, brands must immediately act on the regional intelligence derived from this peak shopping period. More analysis is forthcoming, but the initial strategy demands immediate attention. For the Americas (AMR), brands must now double down on loyalty partners and capitalize on the remaining high average order value (AOV) window. For EMEA, campaign efforts must urgently focus on arresting the return on ad spend (ROAS) decline that preceded Black Friday. The next ten days are critical for establishing momentum before the major holiday purchasing peaks arrive.

For even more holiday performance highlights, visit our holiday content hub right here.