Many people have asked about what we are seeing in the aggregated data for partner and affiliate programs worldwide and by category of advertiser.

To find out, we’ve examined the March 2020 data for all programs in order to provide insights into how the industry is responding to the current uncertain situation. We also asked our Client Success and Partnerships teams about the topics that they are discussing most as they reach out to their counterparts.

WHAT WE ARE SEEING IN THE DATA

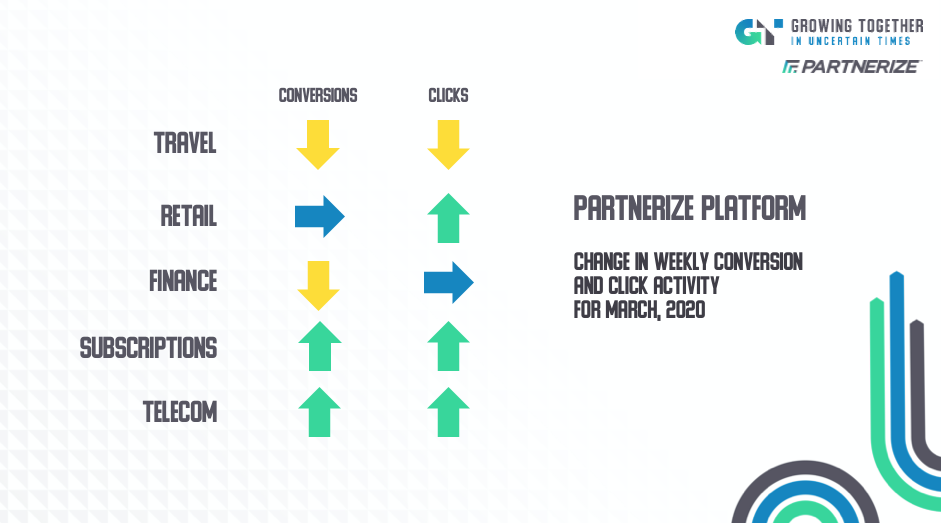

We compared weekly sales for the last weeks of February with weekly sales during March to identify significant changes in activity.

Not surprisingly, some sectors are down significantly, but there are also bright spots, and we expect to see more of those over time as we all adapt.

Our 300+ advertisers are not necessarily representative of the market in total, but they can provide visibility into what a big sample of large advertisers is doing in response to the time. We have omitted data from clients that do not wish us to share insights even in this very aggregated form.

As you can imagine, daily and weekly data are quite volatile. Short-term promotions, holidays, and other market events impact both the rates of click and conversion in our industry. Nevertheless, we have endeavored to provide some insights below, after allowing for the noise.

TRAVEL

Not surprisingly, the Travel vertical has been hit hardest by the current situation. With many hotels completely closed, and airlines either grounded or flying very limited schedules, we’ve seen conversion declines of more than 80% over the course of the past month. Clicks are down as well, but not as steeply. There are a few advertisers in our sample that have continued small programs where domestic travel remains open. But many programs are significantly reduced or on pause until the situation normalizes.

RETAIL

By contrast, the retail sector is performing much better. Over the course of the month, we have seen fairly flat Retail conversions (up 2%) over the period. We’ve seen a much larger increase in retail clicks for the period, up more than 33%. This would seem to indicate that people are shopping more but that the number of actual purchases across all of our advertisers is holding fairly steady.

Retail sectors performing best in our sample are:

- Beauty and Personal Care, where we have seen a 33% increase in conversions and a 42% increase in clicks.

- Luxury, where we’ve seen a 16% increase in conversions and an 8% rise in clicks

- Apparel, where we have seen an 8% increase over the period in weekly conversions, with clicks increasing 10%.

FINANCE

Data for Finance have been highly variable for the period. Overall, activity in the category is pretty stable, holding flat for much of the month but down in the last two weeks. But weekly variances (up AND down) are quite high.

Some brands have increased their investment in the sector, likely diverting other marketing investments into pay-for-performance. Other brands have slowed or paused. Because there has been so much market and financial volatility, we will report specifics on this sector in the coming weeks, when we have more information.

SUBSCRIPTIONS

We work with a number of online entertainment and information companies that sell subscriptions. Overall, we’ve seen a 30% increase in conversions month over month, and a 48% increase in clicks. Naturally, performance varies significantly by provider and the extent to which they rely on live programming as part of their model.

TELECOMS

We work with 10 of the largest telecoms worldwide, many of which provide products and services in trading regions where populations are under stay-at-home rules. Globally, we’ve seen a 5% increase in conversions month over month, and a 6% increase in clicks.

WHAT WE ARE COLLABORATING ON

Our CS and Partnerships teams are reaching out every day to help provide insights and ideas that can help all stakeholders in partnership get better results. Our goal is to help people find real solutions to challenges and new opportunities so they can avoid rash decision-making and instead make informed, creative choices.

Here are some of the major themes we are discussing.

MORE CONSIDERED RESPONSES: In the first days of the crisis, we were seeing some brands and partners take abrupt actions like pausing programs or cutting commissions without warning. This has been widely noted across the industry. Those sorts of abrupt changes have become less common in the last two weeks as brands recognize the importance of strong long-term relationships and the benefits of continued investment in pay-for-performance partnerships. They still happen, but less often.

MORE COMMUNICATION: We’re seeing more brands and major partners reaching out to one another to discuss issues and opportunities. We are also seeing more partnership teams selling the value of the channel to internal leaders so that there is a broader understanding of the pay-for-performance and other benefits. We urge our clients to stay in close touch with their major partners so they can collaborate and develop new ideas to solve short-term and long-term problems.

BESPOKE PROGRAMS: Our CS team is working with a number of brands on specific new partnership campaigns and offers to meet their immediate challenges. We are providing ideas and support for programs that turn brand employees and loyalists into Brand Ambassadors. This can help increase AOV, drive sales when inventories are uneven, and address challenges with high return rates. To provide additional assistance here, we will be offering webinars in all regions on specific ways to meet immediate needs. Watch this blog and your inbox for an invitation.

RELAXATION OF PARTNER RULES: Some large partners are relaxing rules like minimum commitments in order to make it easier for brands to work with them. This speeds time to revenue for everyone.

PARTNER RECRUITMENT: While some brands have cut or paused partnership activity, others are beginning to talk about expanding programs with more partners and new classes of partners. This is a win-win for both brands and partners, and our Partner Discovery and Brand Discovery solutions are seeing significantly increased trial/usage. These two offerings help brands and partners respectively identify new relationships with a high degree of likelihood to deliver results at scale. Brands should be assured that there are lots of great partners out there ready to go to work on their behalf.

Our teams are reaching out regularly to clients and partners alike to help them navigate these strange times. Contact your CS or Partnerships lead to discuss your own goals and needs today.

FINAL THOUGHT

The data and findings above are for a relatively short period of time, but they provide a glimpse at the relative reactions of some of the largest verticals in the space. In future weeks we will work to examine performance by region and other metrics. Fortunately, one of the most powerful ways that we can all respond to this is to work together – to grow together in uncertain times.