Occasionally, our partners and clients submit posts to our site for publication. We are pleased to publish a range of these opinions, which reflect the POVs of the author(s). This time, we welcome Anthony Quinn, Managing Director at Lodestar.

Southeast Asia is catching up fast when it comes to e-commerce and interest in utilizing the affiliate channel to grow businesses. In this two-part blog series, we’ll be examining market size compared to the US and UK markets as well as some nuances to be prepared for when conducting business in Southeast Asia (SEA).

Asia overall (including China) is now the largest B2C e-commerce market globally, ahead of the US and Europe. The growth and sheer size of major online marketplaces here such as Alibaba, Lazada and Shopee demonstrates that changes in shopping behaviours of consumers in this region are happening at a rapid pace.

When broken down and excluding China, Southeast Asia (SEA) is home to a population of 583 million, with the major economies spread over six main countries (Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam). These countries all have their own unique cultures, history, shopping behaviours and ways to do business.

SEA is also a huge market, and currently, quickly moving online. As of 2020, 70% of the population or 400 million people in this region are online, an increase of 40 million compared to the year before. This growth in internet users has been led especially by Indonesia, who house the largest population out of these six key economies.

The ‘COVID-19’ effect

Consumers here took a different approach to their behaviour during the initial outbreak, mainly due to cultural and behavioural differences. People in these countries took greater heed to the governmental advice with regards to social distancing, the wearing of masks and especially the advice to stay at home as much as possible. This was clear in Bangkok where Lodestar Marketing is based, as the city became a ghost town overnight! Brick and mortar stores clearly suffered as a result.

However, with the population house-bound for this extended period of time, it led to a significant change in behaviour: Online shopping boomed, while the number of hourly internet users nearly doubled during lockdown.

Consumer buying power is still less than in more developed regions. One important note to make is the difference in buying power here. How much on average do consumers in these markets spend compared to the US and UK? The differences are significant.

When looking at the purchase of consumer goods, annual SEA per-capita spend is still much lower compared to other major regions worldwide. The average shopper in SEA spends less than a quarter of the global average (except in Singapore). The Philippines ranks bottom with the lowest average at US $18 per person on average (2018) compared to US at $1,951 and UK at $1,639. Singapore is highest, with an average spend of £1,037. But all other SEA major economies are below the global average of $634 USD.

Ecommerce Growth

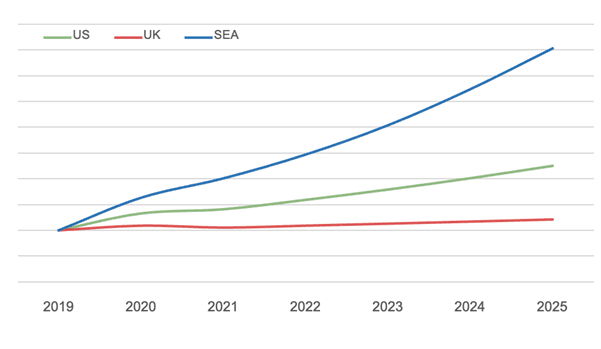

According to a study by Google and Temasek, the online economy (online media, online travel, transport & food plus e-commerce) in SEA is expected to grow from $105bn in 2020 to $300bn by 2025, with an average annual growth rate of 24%. When focusing exclusively on the ecommerce category, growth is forecast to outpace both the US and UK.

Figure 1: Market Growth Forecast (source: emarketer/e-Conomy SEA 2020 Report)

As noted in Figure 1, whilst US growth is forecast at a CAGR of 11% YoY and the UK at 3.5% CAGR, SEA is forecasted to outpace that significantly with an average YoY % growth rate of 23%. Going by the forecast, SEA (a collection of the six main countries aforementioned) is on track to surpass UK by the end of 2024.

Due to the ‘COVID-19 effect’, a growing number of people are now starting to shop online. A report from GlobalWebIndex shows that 9 in 10 users in Indonesia now purchase online every month. This trend is mirrored in all the other key SEA economies—except the Philippines—surpassing the global average of 75%.

Interest in the Affiliate Marketing Channel

It’s not just the sales numbers that are painting a bright picture for this region. According to Google Trends data search interest in the query “affiliate marketing” from the last 5 years has increased at a consistent rate, up over 200% overall compared to the 5 years previous. The query has increased at a lower rate in US and UK, growing 188% and 143% respectively. In the main SEA region, however, the search term volume has increased over 300%. And this doesn’t take into account the local language differences for the same term in countries such as Thailand and Vietnam, so the number may potentially be higher.

What Makes This Region Unique?: Payment Models & Social Media

The majority of online transactions made by consumers in the US and UK involve card payments at 47% and 53% usage penetration respectively. In the UK, PayPal was the most used online payment method in 2019. According to the 2019 survey by Attest, 49% of shoppers were using their PayPal accounts to make payments, while 37% used a credit or debit card. This is not the case so much in SEA (except for Singapore). Bank transfers and Cash on Delivery (COD) are still very popular.

Having established that, payment by card in Thailand is the dominant payment method, responsible for 30% of total transactions. This is initially surprising considering that the overall card penetration rate is less than 1% per capita. But it is interesting as it gives an indication of the dominance of the middle class that are driving transactions online. And although 30% seems high for a country still in the very early stages of e-commerce adoption, it does get skewed somewhat towards a lower percent when you factor in social commerce. There are no official or accurate numbers on how much ecommerce is driven by this channel, but it is estimated that it could be as much as 30-40%. And these payments are almost all done via bank transfer.

Consumers in Thailand are still generally more comfortable paying for goods online via social media. In other words, they prefer to pay cash to someone selling on Facebook and entrusting them to deliver the items – rather than purchase with an ecommerce retailer with a secure payment gateway! Facebook has recently announced the launch of Shops, allowing consumers to purchase through social media sites such as Facebook, Instagram and even via Whatsapp. This is great news in terms of being able to measure this channel more effectively but whether this will affect e-commerce via other channels remains unseen.

It is also worth noting that the adoption of digital wallets is on the rise. It is almost as if SEA skipped over the adoption of card payments to set up using e-wallets as their primary form of electronic payment. SEA is leading the way globally with a predicted annual growth rate of 8%. If this trend continues, there will be over 65% of consumers using e-wallets as their preferred payment method by 2023. Indonesia is leading the way with 72% of transactions made with an e-wallet. In comparison, usage of e-wallets in the UK and US is just under 30%.

The high adoption rate of e-wallets can be linked to the well-known trend that this region is a ‘mobile first’ region, with most having access to the internet and as e-wallets are typically tied to their devices, it makes it easier to pay using a smartphone. Once again, Indonesia leads the way, with almost 80% of the country’s internet users aged between 16 and 64 reporting that they bought something online via a mobile device in the past month. Thailand comes in second at 74%, while the Philippines and Malaysia both see mobile commerce adoption rates in excess of 60%. At 58%, Vietnam is ahead of the global average of 52%, while Singapore comes in just below that average, at 51%.

Key Dates & Campaigns

Move over Black Friday, there is a new campaign in town!

By far the biggest shopping day in this region (and now globally, thanks to the huge sales driven by Alibaba alone) is 11.11 (11th November) or ‘Singles Day’. The term was originally coined in China as the date matches with four ‘ones’, representing four singles. In 2020, 800m shoppers globally participated in sales during this day. The most popular product categories for Singles Day in SEA were apparel and accessories, whereas in the US for Black Friday, computing/high tech is still at the top of the tree.

Following this, the largest marketplaces in SEA, Lazada and Shopee, have taken this to another level. First, there was 12.12, then 10.10 and then, well, you get the picture. Now there are monthly sales based around those dates which most stores have now adopted as part of their campaign calendars.

Another key date for this region is Chinese New Year, where campaigns are known to run for two or three weeks. As a result, sales start to increase approximately three weeks before the actual holiday starts. Sales in grocery, a top selling category, were boosted online especially due to the pandemic. However, other stores jumping on the campaign bandwagon saw success with other types of products such as clothing, electronics, smart home appliances, and health care products. According to Criteo, there’s a daily increase of 71% in fashion, 101% in grocery, and 56% in sales for beauty products during the period across the East Asian region.

Live Commerce

Live commerce has become an increasingly important and fast-growing marketing channel in which to drive sales. It is basically like a shopping channel but streamed and promoted via major social media networks (Facebook live, for example).

It boomed particularly in 2020, with order volume from live stream shopping growing by around 115% across Thailand, Vietnam, the Philippines and Singapore. But again, the increased popularity and success of this channel has been fueled by people looking to shop online as an alternative to offline, which has been greatly affected by the pandemic.

Summary

SEA is a remarkably diverse region with a huge demographic and socio-economic differences. Household incomes vary wildly from high incomes in Singapore to lower incomes in Vietnam; ultimately underscoring the width and depth of the opportunity at hand. As such, each of the markets across Southeast Asia contain millions of online shoppers ready to buy, an explosive growth balanced with traditional preferences like cash on delivery. In the US, e-commerce is now on track to surpass 20% of total retail by 2024, and the UK is forecast to reach nearly 30% of total retail by then. This bodes well for SEA, clearly showing that online shopping can continue to increase their share of the overall commerce pie.

So what’s next for Southeast Asia? Stay tuned for the second part of this guest blog series where we’ll take a look at what’s in store for the rest of 2021.

About Anthony Quinn

Anthony is one of the Managing Partners of Lodestar Marketing. He is a seasoned digital marketeer with long-standing experience within the affiliate channel, having worked in the industry for over 20 years. He has worked advertiser-side with GAME, the UK’s largest specialist video games retailer, at Rakuten Affiliate leading half of the Advertiser Services team and as a publisher at RebateMango, SEA’s most rewarding loyalty platform.

About Lodestar Marketing

Lodestar Marketing is the only specialist Affiliate Marketing Management agency in Southeast Asia. The founders collectively have over 35 years+ experience in the channel and spent the best part of the last 10 years in this region so are perfectly suited to grow affiliate marketing programs, whether new to the channel or are looking to analyse and grow existing programs. Discover more at https://lodestar-marketing.com.